*Please note that due to an internal reorganization this rebranded Voluntary Carbon Market Outlook report will be sent from info@redshawadvisors.com from next month onwards. Please add the address to your contacts to ensure you receive it or please contact us if you have any questions on this.*

- Carbon Credit Issuance, Retirements Prices start 2023 on a week note

- The nature-based premium is eroded, but only for standardized products

- A Guardian article about the validity of REDD+ projects sparks debate

- Core Carbon Principle (CCP) publication now expected in March

- The UK's net zero review provides encouragement for carbon removals

What you need to know

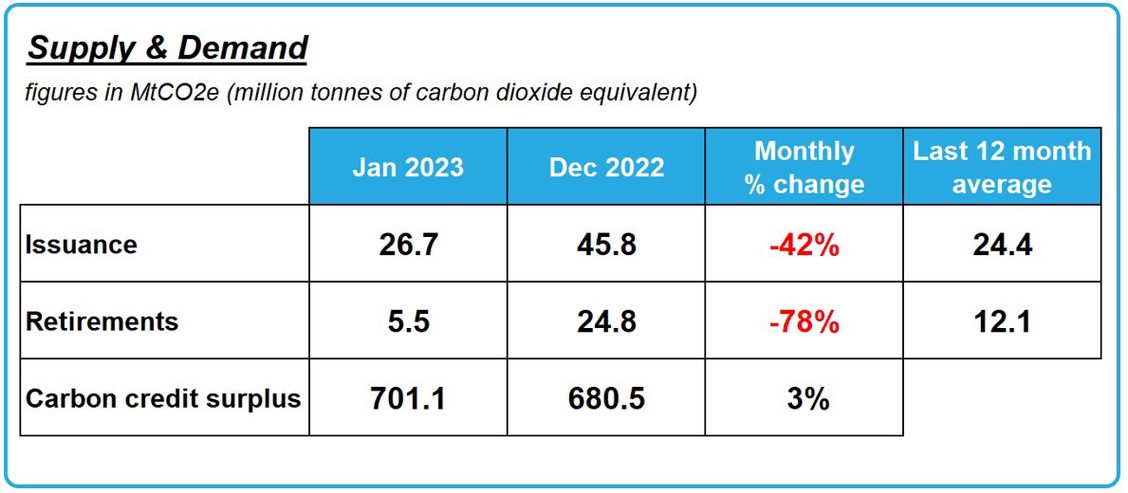

Carbon credit issuance and retirements fall after December spike

In January, carbon credit issuance and retirements fell from strong December figures. However, whilst the 27Mt (million tones of carbon dioxide equivalent) of issuance was slightly higher than the 2022 yearly average, retirements dropped to 5.5Mt, less than half of the 2022 average.

The slow start to the year in terms of retirements was partly expected as many corporates retired credits for calendar year-end in December, leading to a record high of 25Mt retirements.

However, many corporates continue to sit in ‘wait and see’ mode as the market continues to suffer from accusations of greenwashing and awaits governance guidelines (from the IC-VCM, read further down for more on this).

Additionally, the effect of the Guardian’s criticism of the VCM (read down more on this) further undermines confidence in the market.

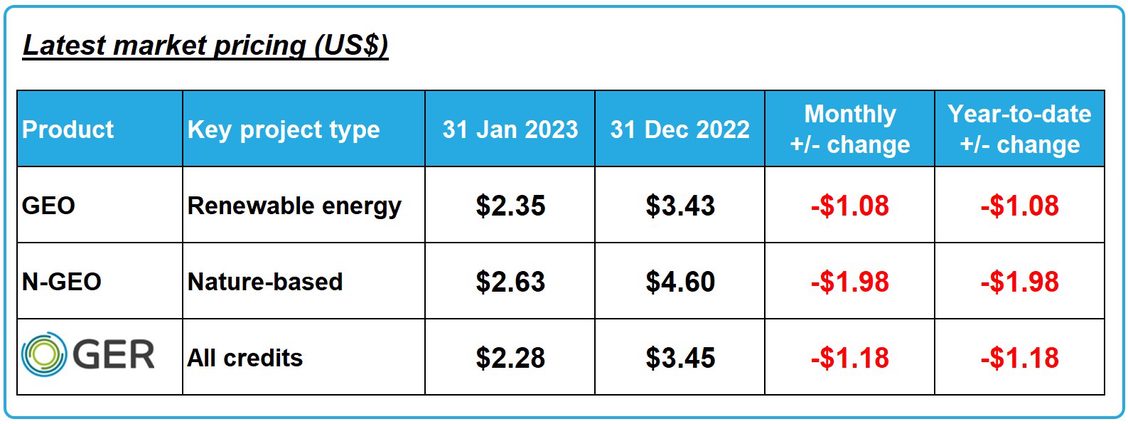

Prices continue to slide

Continuing in the same vein as 2022, carbon credit prices fell across the board. A host of standardized VCM products dropped in excess of 30%.

Prices in the bilateral over-the-counter (OTC) market fared considerably better than the standardized products. There are a number of reasons for this:

1. The standardized contracts are ‘sellers option’ contracts and so buyers do not know which carbon credits they will receive until the contract expires and becomes deliverable. Any project (including those targeted by greenwashing claims) can be delivered into these contracts as long as they meet the minimum criteria.

2. Several of the contracts have been designed with traders in mind, rather than end users. As a consequence, the standardized product space experiences more volatile price fluctuation.

3. The only ultimate buyers of carbon credits are corporates wishing to make carbon neutrality claims. In an environment of greenwashing fear, not only will buyers shy away from the market but they will be more keen than ever to know about what they are buying. Thus, OTC prices for projects perceived as ‘high-quality’ are pricing way above the standardized products.

However, there are very few, if any voluntary carbon credit prices that have been immune to the loss of confidence in and drop in value of the VCM.

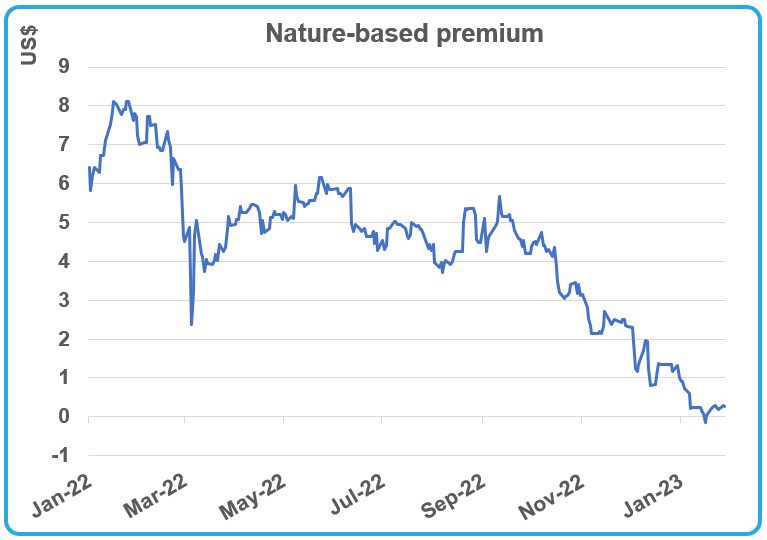

Are nature-based projects still priced at a premium?

In terms of project category pricing, nature-based carbon credits have long traded at a premium to the other largest carbon credit category: renewable energy. A crude representation of this ‘nature-based premium’ can be found through comparing standardized product prices (where these categories comprise the majority of the eligible pool of credits).

Around a year ago (per the graph below), the ‘nature-based premium’ shown by this measure reached US$8 per carbon credit.

The premium has slowly eroded over the last year and in January, it momentarily inverted.

However, whilst the advent of standardized products has enabled greater transparency of carbon credit prices, this method of calculating the nature-based premium is not without its limitations.

A specific caveat is that the standardized product prices will closely track the lowest value credits which meet the specifications. When one considers the criticism which REDD+ projects have been subject to in the recent past, this is a key driver of the change in the premium and we still observe many forestry based projects trading at a large premium to renewables projects in the OTC market.

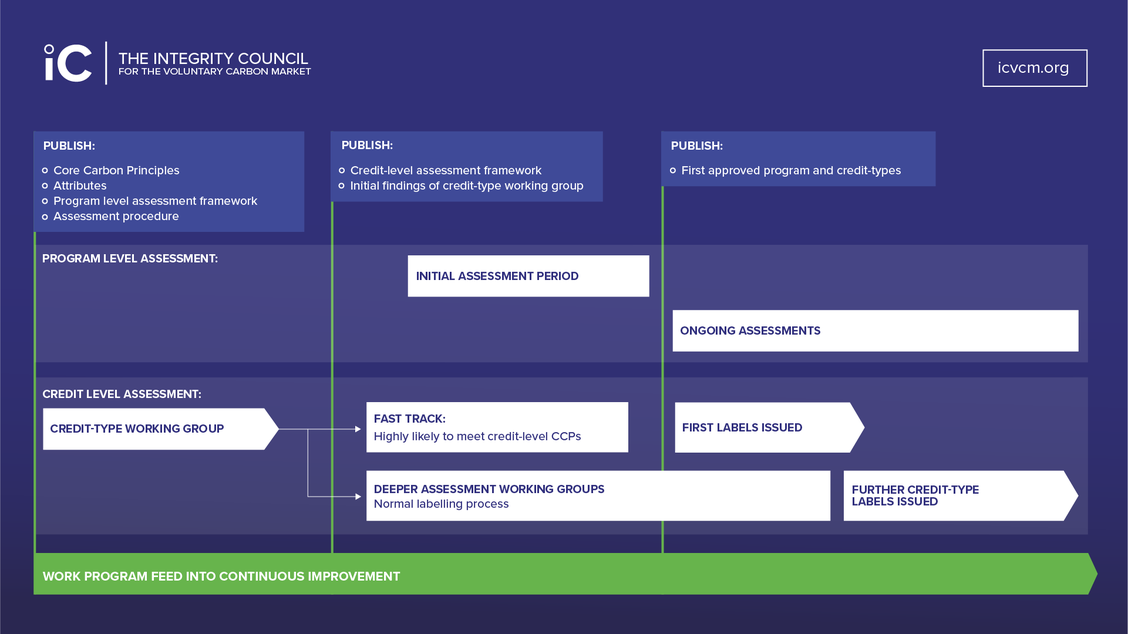

Core Carbon Principles (CCPs) to be published in March

The Integrity Council for Voluntary Carbon Markets (IC-VCM) is a quasi-regulatory private body working on VCM governance. In January, the IC-VCM published a new timeline with two key dates:

- March 2023:Publish the final Core Carbon Principles (CCPs)

- Q323:Label the first approved programmes and credit types with CCP approval

A remaining concern of stakeholders is that the stringency of the CCPs could mean that very few existing carbon credit projects would pass the IC-VCM’s test.

This could undermine the VCM’s credibility and prospects for growth if the available supply of what companies are told they should buy is too low.

A market needing a boost to its trustworthiness?

The work of the IC-VCM and its potential impact has possibly been brought into the spotlight more than ever, following the January publication of an article by the Guardian (in partnership with Die Zeit and Source Material). The piece was emblazoned with the sensationalist headline of ‘Revealed: more than 90% of rainforest carbon offsets by biggest provider are worthless’.[1]

The article refers to three studies undertaken to review projects which have issued REDD+ carbon credits through the largest voluntary standard, Verra. It claims that ‘Only a handful of Verra’s rainforest projects showed evidence of deforestation reductions’.

At the end of January Verra responded in detail, through a technical review of the article and the studies on which it was based.[2] It believes that the investigation ignores “project-specific factors that cause deforestation” and that, as a result, “these studies massively miscalculate the impact of REDD+ projects”.

As is its modus operandi, Verra reviews criticism of its projects and updates its methodologies when it finds shortcomings which it sees as necessary to address. Through this process, Verra has identified the need to transition all REDD+ projects on to a new consolidated, jurisdictional REDD methodology.[3]

In our quarterly report for paid subscribers, we will provide a more detailed look into the topic of REDD+ and why it has become one of the most divisive carbon credit categories.

Contact us at info@redshawadvisors.com to discuss our research, training and advisory offerings.

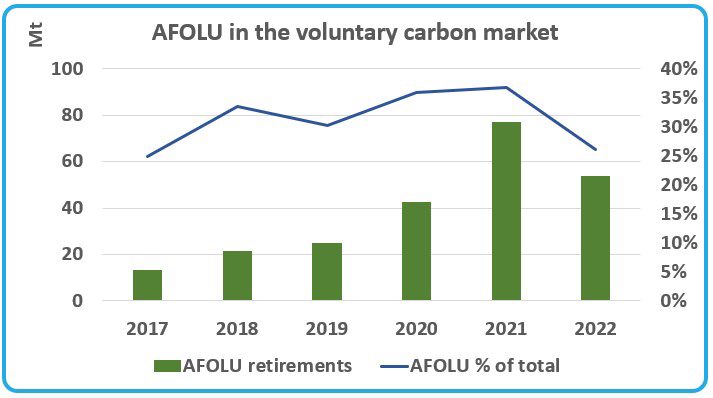

Further concerns afflict the forestry carbon credit category

Since the Guardian article was published there has been a huge number of VCM participants and commentators weighing in with differing viewpoints. Whilst technical arguments are sure to rumble on, there is little doubt that the criticism and debates will further weigh on the REDD+ project type category which had already suffered a steep decline in retirement levels in 2022.

Last year, retirements of REDD+ carbon credits sharply fell to 21Mt in total, from 33Mt the prior year. This was the significant driver behind the drop in retirements from the Agriculture, Forestry and Other Land Use (AFOLU) project category.

Other VCM developments which caught our eye last month

Carbon Removals: The net zero subsidy race heats up as EU president Ursula Von Der Leyen announces a plan to compete with the United States’ Inflation Reduction Act (IRA). The IRA significantly improved tax breaks to support carbon dioxide removal. This has been formalized in early February through the EU’s Green Deal Industrial Plan.

Carbon insurance: Reinsurer Chaucer announced a partnership with carbon credit insurance specialist Kita to help provide insurance for delivery risk to carbon credit buyers.

Compliance and voluntary market links: The UK’s independent net zero review recommended that a path was charted to address the inclusion of GGRs (Greenhouse Gas Removals) in the UK ETS (Emissions Trading Scheme).

Redshaw Advisors offers a range of services across the compliance & voluntary carbon and renewable energy markets to help companies navigate their environmental market risk.

Contact us info@redshawadvisors.com to learn more about our environmental market services.

References

[1]https://www.theguardian.com/environment/2023/jan/18/revealed-forest-carbon-offsets-biggest-provider-worthless-verra-aoe-

[2]https://verra.org/technical-review-of-west-et-al-2020-and-2023-guizar-coutino-2022-and-coverage-in-britains-guardian/-

[3]https://verra.org/revision-of-verras-avoiding-unplanned-deforestation-and-degradation-project-methodologies-update-

法人様向けの有料プログラム

有料サービスに申し込むコメント投稿や閲覧が可能

無料会員に登録する既に会員のかた

ログインする